Today, I can’t help but notice some of the striking similarities when it comes to Visa (V) and MasterCard (MA). Just like Coca-Cola, they are cash cows with solid fundamentals and have a high barrier to entry (their moat is deep). But most impressive is their limited saturation in the emerging markets, which are just now undergoing the transition from cash to credit cards.

Let’s take a look at a few of their key stats as of February 22, 2011:

| Visa | MasterCard |

| Marketcap: 52.57B Trailing P/E: 17.03 Forward P/E: 13.12 PEG (5 yr expected): 0.83 Profit margin: 37% | Market Cap: 32.38B Trailing P/E: 17.61 Forward P/E: 12.67 PEG (5 yr expected): 0.75 Profit margin: 33.33% |

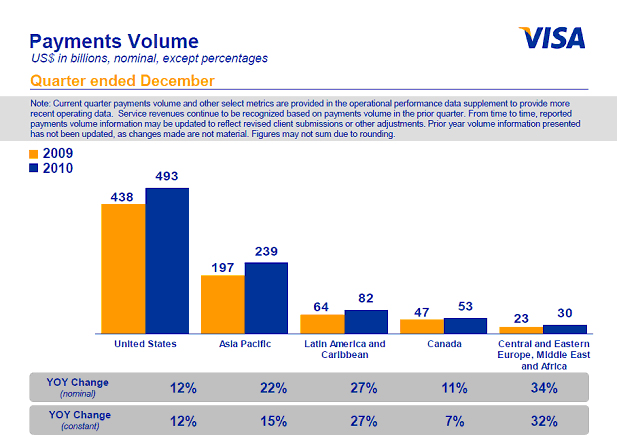

Right now only around 40% of Visa’s revenue comes from overseas, yet that is where 60% of the growth from last quarter came from. By the looks of this chart below, it’s easy to understand why:

[Click to enlarge]

Visa YOY Growth - Source: Visa.com

Visa YOY Growth - Source: Visa.comOn the other hand, more than half of MasterCard’s revenue comes from overseas, but its international growth closely mimics Visa's.

Lower risk than banks?

We all know what happened to the banking industry during the recession, but Visa and MasterCard were relatively unscathed. Why? Because all they do is process payments; they don’t actually issue cards or extend credit. Taking a cut from each transaction -- but not enduring the risk associated with extending credit -- doesn’t sound like a bad deal, does it?

Conclusion

Although American Express (AXP) and Discover (DFS) are commonly accepted cards in the United States, when it comes to most developing countries, Visa and MasterCard practically have monopolies. So not only do they enjoy an international stronghold with a strong barrier to entry, but they are also riding two powerful trends:

- The switch from paper currency to debit/credit cards.

- Massive growth opportunities in developing markets.

URL: http://seekingalpha.com/article/256021-visa-and-mastercard-credit-card-plays-worth-a-look

No comments:

Post a Comment